Summary

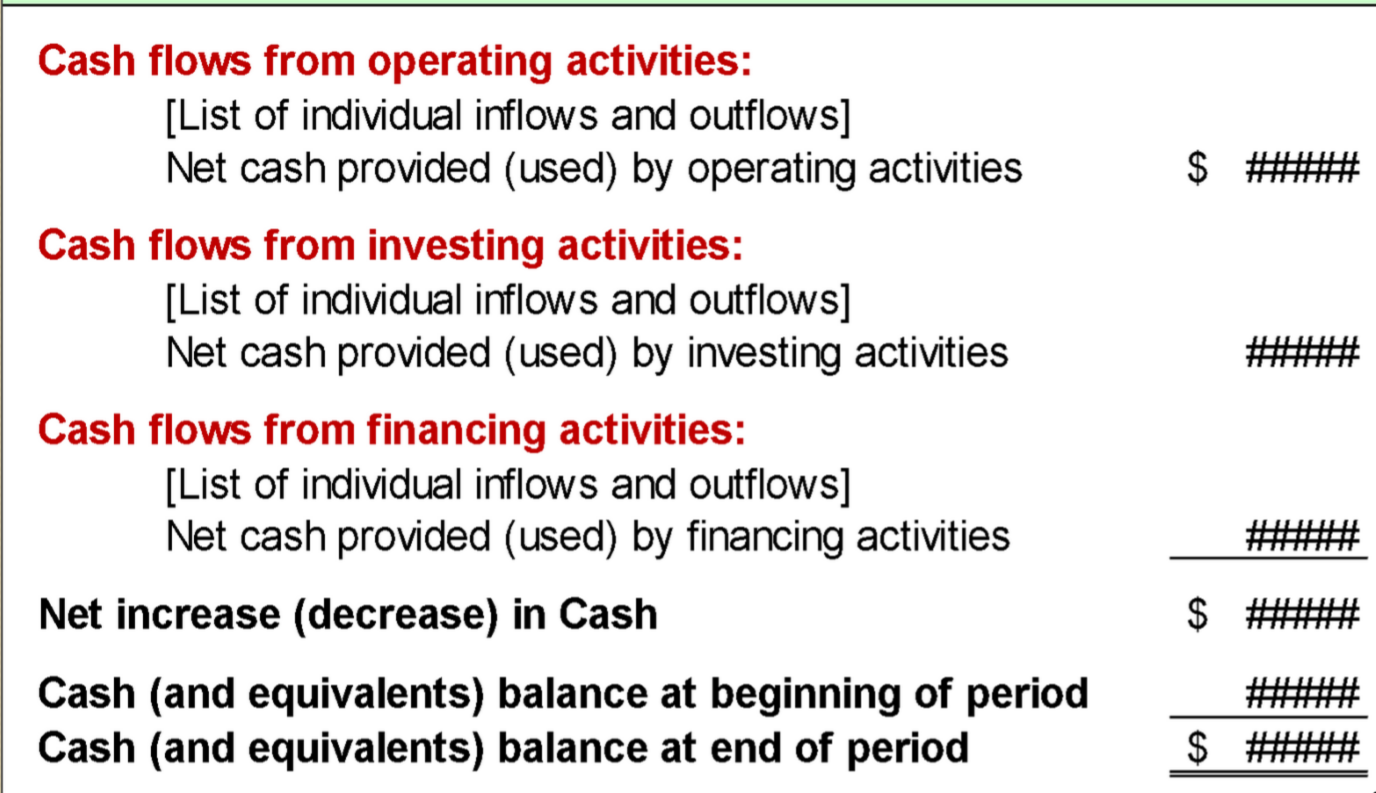

Statement of Cash Flows

Layout of Statement of Cash Flows:

Cash Flows from Operating Activities

- Inflows (+):

- interest and dividends received

- sales to customers

- Outflows (-):

- suppliers of merchandise and services

- employees

- lenders for interest

- governments for taxes

Cash Flows from Investing Activities

An investment is any use of cash today with the expectation of receiving a return (profit) in the future. By lending money, you are “buying” a Note Receivable—a long-term asset.

- Inflows (+):

- Sale of investments and plant assets

- Collection of principal on loans

- Outflows (-):

- Purchase investments and plant assets

- Purchase debt or equity investments

- Make loans

Cash Flows from Financing Activities

When you repay the principal of a loan you took out, it is considered a financing activity.

- Inflows (+):

- Short-term and long-term borrowing

- Owners, i.e. from issuing stock

- Outflows (-):

- payments on borrowed

- owners (i.e. dividends, stock repurchase)

- purchase treasury stock

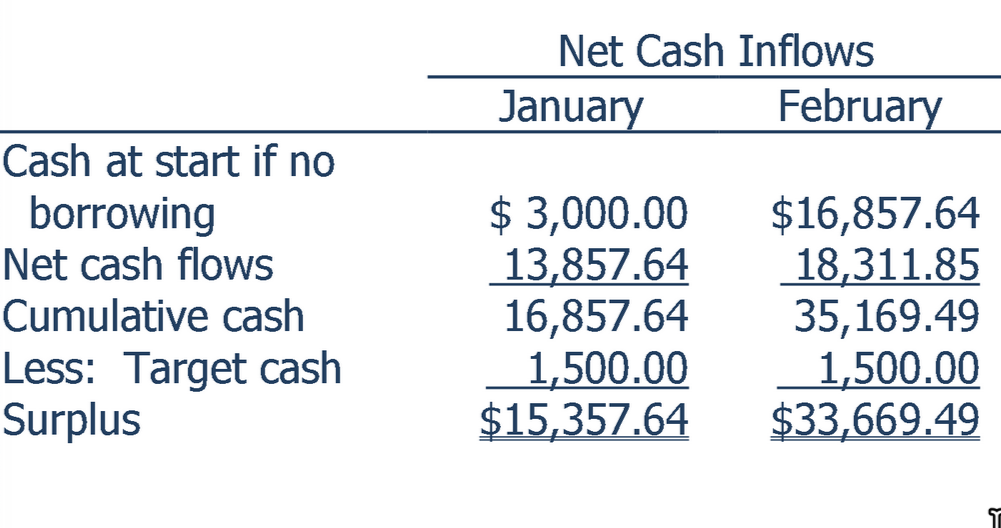

Cash Budget