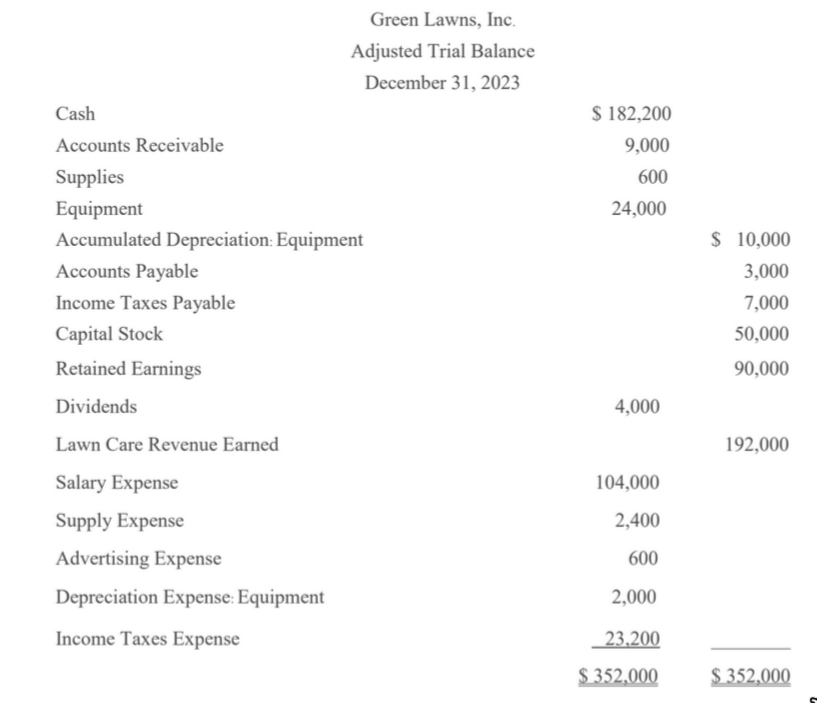

Summary

Adjusted Trial Balance

Report of all account balances before the formal Financial Statements are created.

Purpose

To verify the equality of total debit and credit balances after adjusting entries are made at the end of the accounting period.

1. The 2nd Column (The DEBIT Column)

Accounts in this column generally represent where the money went or what the company owns.

Values appear here if the account is:

-

An Asset: Things you own (e.g., Cash 9,000, Supplies $600).

-

An Expense: Money spent to run the business (e.g., Salary Expense 600).

-

Dividends: Money paid out to owners/shareholders (e.g., Dividends $4,000).

2. The 3rd Column (The CREDIT Column)

Accounts in this column generally represent where the money came from (the source of the funds).

Values appear here if the account is:

-

A Liability: Money you owe to others (e.g., Accounts Payable 7,000).

-

Equity: The owner’s investment or kept profits (e.g., Capital Stock 90,000).

-

Revenue: Money earned from customers (e.g., Lawn Care Revenue $192,000).

-

Contra-Assets: This is a special category. Accumulated Depreciation ($10,000) is in this column because it “offsets” or reduces the value of an asset (Equipment).